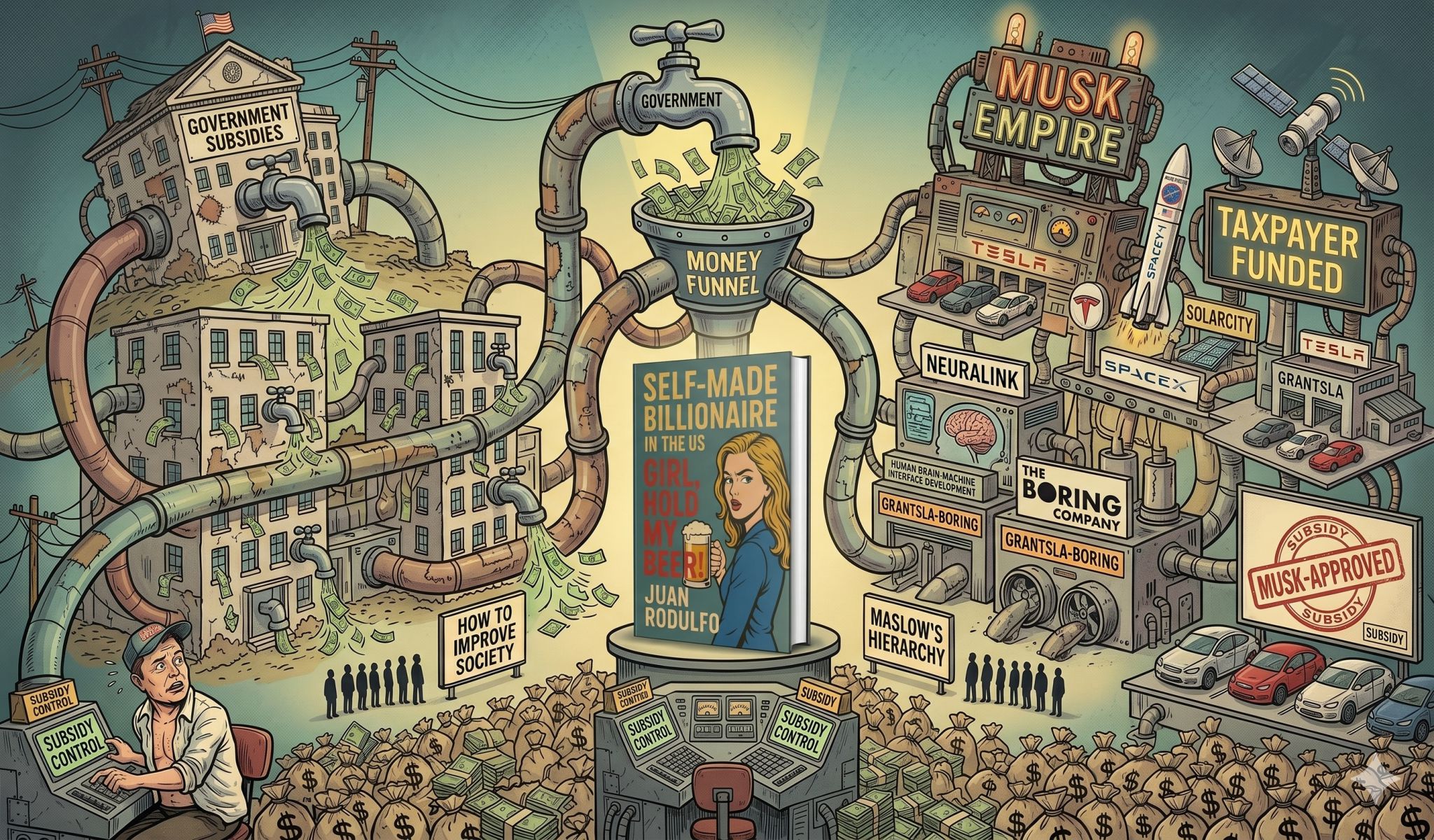

Corporate Welfare: The Government Subsidies Behind the Musk Empire July 12, 2026June 5, 2026 by Juan Rodulfo Share this:Corporate Welfare, Government Subsidies, Elon Musk, Tesla, SpaceX, Taxpayer Funds,

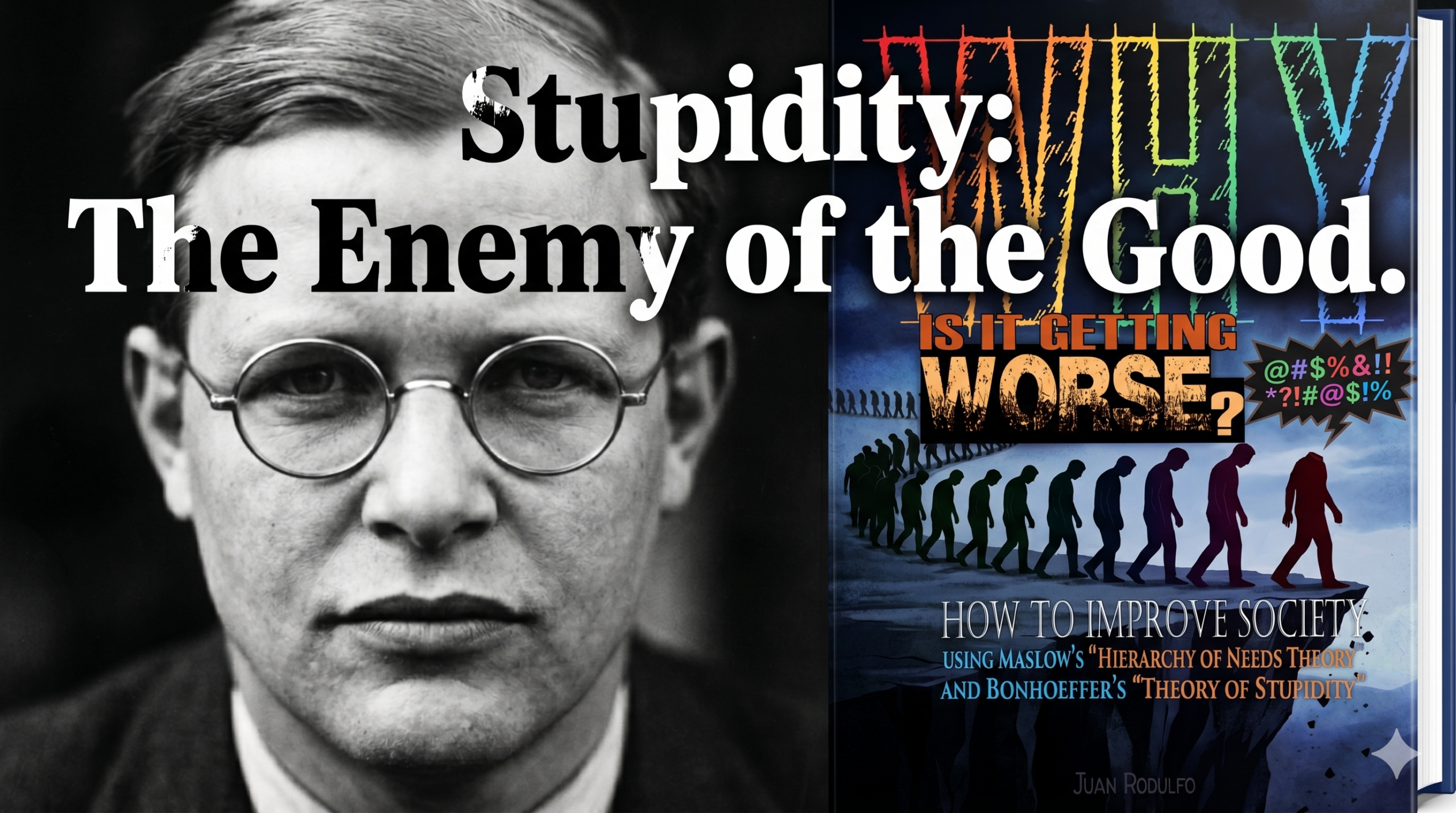

The Most Dangerous Human Trait: Bonhoeffer’s Theory of Stupidity June 2, 2026 by Juan Rodulfo Share this:Dietrich Bonhoeffer, Theory of Stupidity, Critical Thinking, Social Manipulation, Groupthink, Psychology of Power, Moral Philosophy,

Rebuilding the Foundation: Is Our Hierarchy of Needs Collapsing? June 2, 2026 by Juan Rodulfo Share this:Maslow’s Hierarchy, Survival Mode, Mental Health 2026, Economic Stability, Self-Actualization, Social Reform, Community Resilience,

Traveling to Abu Dhabi: Where Culture Meets Modern Luxury May 26, 2026 by Juan Rodulfo Share this:Abu Dhabi travel, UAE tourism, Sheikh Zayed Mosque, Louvre Abu Dhabi, Yas Island, Corniche Beach, Qasr Al Watan, Saadiyat Island, Liwa Desert, Abu Dhabi attractions,

The Secret to a Happy, Focused Dog: Why These Lickable Squeeze Treats Are a Game-Changer May 25, 2026 by Juan Rodulfo Share this:Dog Treats, Lickable Dog Treats, Pet Enrichment, Puppy Training, Dog Food Topper,